Variable Costs and Fixed Costs

All the costs faced by companies can be broken into two main categories: fixed costs and variable costs.

Fixed costs are costs that are independent of output. These remain constant throughout the relevant range and are usually considered sunk for the relevant range (not relevant to output decisions). Fixed costs often include rent, buildings, machinery, etc.

Variable costs are costs that vary with output. Generally variable costs increase at a constant rate relative to labor and capital. Variable costs may include wages, utilities, materials used in production, etc.

In accounting they also often refer to mixed costs. These are simply costs that are part fixed and part variable. An example could be electricity--electricity usage may increase with production but if nothing is produced a factory still may require a certain amount of power just to maintain itself.

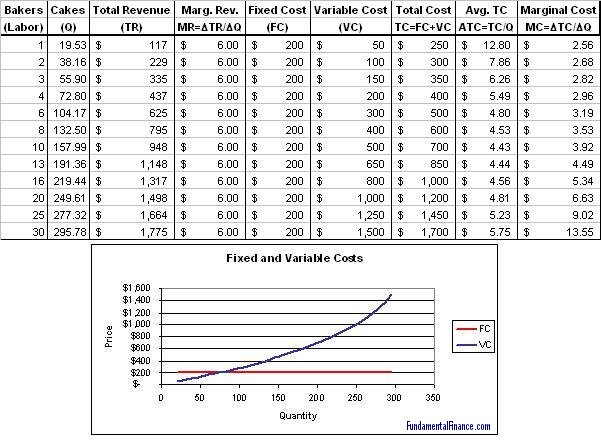

Below is an example of a firm's cost schedule and a graph of the fixed and variable costs. Noticed that the fixed cost curve is flat and the variable cost curve has a constant upward slope.

|